KEMSA has kicked off a two-week national stocktaking exercise to verify

Safaricom has rolled out yet another pathway of turning loyalty into impact

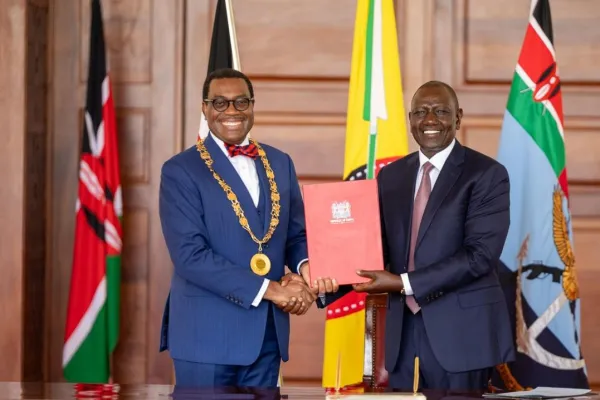

Kenya and the United Kingdom have unlocked a major investment pipeline worth