Firms hit as fuel price shock sparks sharpest cost inflation since 2023

Currently, petrol is retailing at KSh197.60, diesel at KSh206.84, and kerosene at KSh 152.78 per litre in Nairobi.

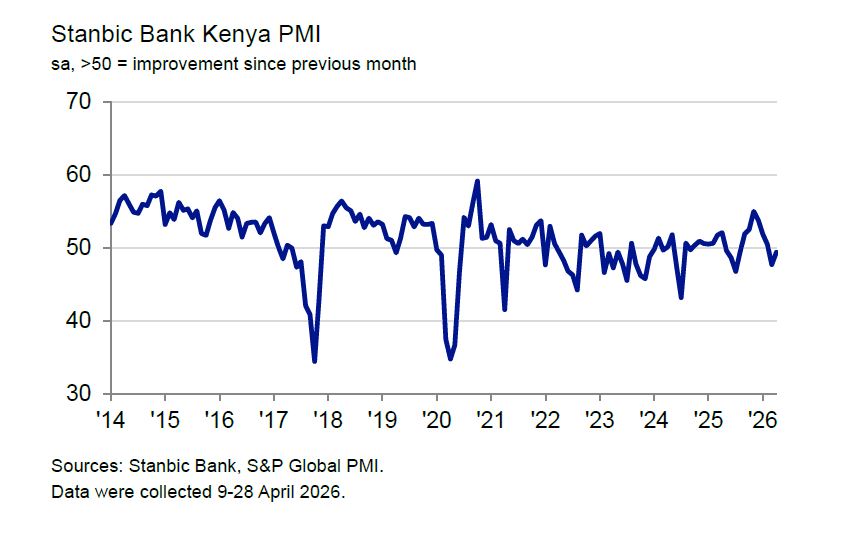

Players in Kenya's private sector experienced a deterioration of the trade environment in April as a steep rise in cost of fuel triggered the sharpest jump in cost inflation since 2023.

During the month under review, Stanbic Bank Purchasing Managers' Index (PMI) edged up to 49.4, up from 47.7 recorded in March, reflecting sustained dip in business activities in the country's private sector. The PMI, remained under the 50.0 neutral mark for the second month in a row.

Related

Kenya's private sector contracts as war in the Middle East hits demand, input costs

Iran war threatens to wipe out Kenya's Sh164Bn Gulf exports

Survey data shows that while the headline index showed slight improvement, a deeper analysis exposes intensifying pressure on investors as output and customer orders decreased for the second consecutive month.

Players in Kenya’s wholesale, retail trade, agriculture and services industries experienced the highest declines in output and dip in new orders. Companies surveyed said decline in activity was "associated with a tapering of customer spending due to rising prices."

Low levels of new business

Kenya's economy was thrown into a spin in mid-April when the Energy and Petroleum Regulatory Authority effected a sharp rise in pump prices with petrol rising by KSh25 per litre and diesel by KSh40 a litre. Currently, petrol is retailing at KSh197.60, diesel at KSh206.84, and kerosene at KSh 152.78 per litre in Nairobi.

Firms reported lower levels of new business “often associated with a tapering of customer spending due to rising prices.” The bulk of those price pressures came from higher fuel costs, which respondents associated to the U.S.-Israel war in Iran that triggered increase in oil prices in the global markets since early March.

“Concerns about rising costs, tied to higher transport costs, and the ability to secure supplies, especially from the Middle East and Asia, weighed on output and new orders in sectors such as wholesale and retail trade, agriculture, and services," observed Christopher Legilisho, economist at Standard Bank.

One of the highlight revelations in April was a sharp rise in input price pressures across the firms surveyed. The report shows that the adjusted input prices index hit its highest level since December 2023, with about two in every 10 respondents recording month-on-month jump in expenses compared to just one percent who experienced a decline.

While higher pump prices were the primary driver of cost increases, a rise in transport charges and shortage of materials also drove up expenses, which ultimately were pushed to customers.

At the same time, the output price index also increased to hit its highest point since late 2023. “As expected, prices rose sharply; input and output prices increased due to higher fuel prices and shipping charges because of the conflict in the Middle East,” Legilisho explained, adding: “However, wage costs rose only marginally.”

Employment numbers on steady rise

However, new work opportunities remained a bright spot in April, growing for the 15th month in a row, with firms reporting jump in casual hires for ongoing projects. Businesses expanding into new markets also reported new hires.

Despite the weaker demand environment, purchasing activity increased for the seventh month in a row, though the rate of expansion was the softest in that sequence. More notably, after falling in March, inventories of purchases rose to the greatest extent so far in 2026.

As fears of fuel price shock coursed through the market, some firms reported attempts to "build safety stocks," meaning that they increased their inventory expecting skyrocketing of prices. This means that a significant number of companies could be bracing for a prolonged disruption rather than a quick reversal of high oil prices.

Supplier delivery times improved for the fifteenth successive month, though the rate of improvement slowed from March. The report noted that some suppliers were able to deliver items quicker attributable to easing demand pressures.

Looking forward, forecasts for the next one year dampened for the third consecutive month with just 18 percent of respondents planning to diversify.

Legilisho stated: “Confidence about future business expectations was down month‑on‑month, although some firms remain optimistic about their expansion plans and the increased diversification of products and services.”