Skip to main content

Main navigation

News

Corporate

Markets

Economy

Intelligence

Fact Check

Investigations

Sustainability

Life

Partner Content

Search

User account menu

Log in

Anonymous user menu

Login

Maudhui House

Coming soon!

Economy

•

Jan 20, 2026

Kalahari Cement rolls out Sh25Bn push to triple EAPC capacity

Amsons Group subsidiary says turnaround strategy will see EAPC annual cement output hit four million tonnes even as staff get better pay

Markets

•

Jan 19, 2026

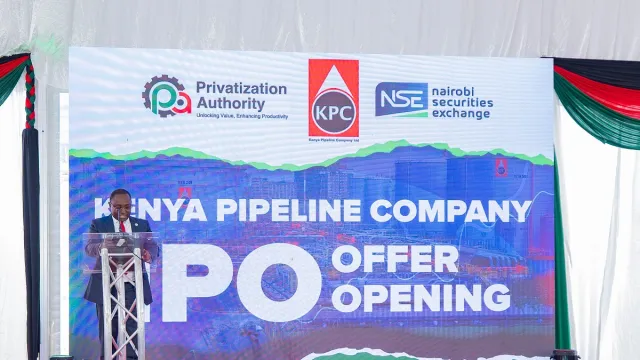

Kenya Pipeline breaks decade-long IPO drought with Sh106Bn ambition

The govt is offering 11.8Bn shares, equivalent to 65% of Kenya Pipeline Company at KSh9.00 per share, aiming to raise KSh106.3Bn from the markets

Economy

•

Jan 14, 2026

AGOA: Kenya gains fresh duty-free U.S. entry until 2028

U.S. House of Representatives has passed a Bill to extend the Agoa, which came

In Summary

Economy

•

Jan 21, 2026

Nairobi stakes claim as Africa’s finance and crypto capital at Davos

Partner content

•

Jan 21, 2026

ABSA returns to power the 5th Sirikwa Classic Cross Country tour

Partner content

•

Jan 20, 2026

Njoroge Kibugu Surges Ahead After Round One of Absa Invitational Series at Karen

News

•

Jan 19, 2026

Safaricom’s sustainability boss Karen Basiye gets global honours for driving social impact

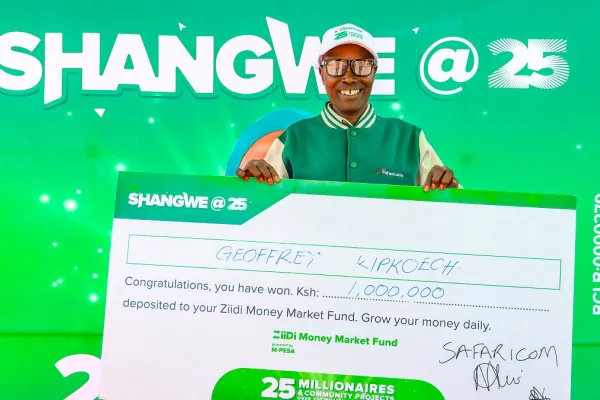

Partner content

•

Jan 16, 2026

Security guard turns millionaire in Safaricom Shangwe @25 campaign

Top Stories

Economy

•

Dec 16, 2025

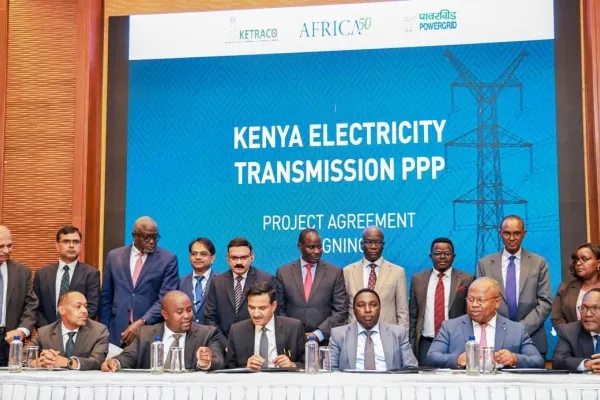

Kenya taps PowerGrid India, Africa50 in Sh40bn grid expansion push

Markets

•

Dec 05, 2025

Vodacom tightens its grip on East Africa with bigger Safaricom stake

Markets

•

Nov 25, 2025

Key dates in the race for a slice of Safaricom’s Sh15 billion green pie

Economy

•

Nov 12, 2025

EAC pilots low-cost, cross-border retail e-payments system

Advertisement

News

View all

News

•

Jan 19, 2026

Safaricom’s sustainability boss Karen Basiye gets global honours for driving social impact

Basiye was honoured for driving forward social and environmental impact within the telecoms industry.

News

•

Jan 12, 2026

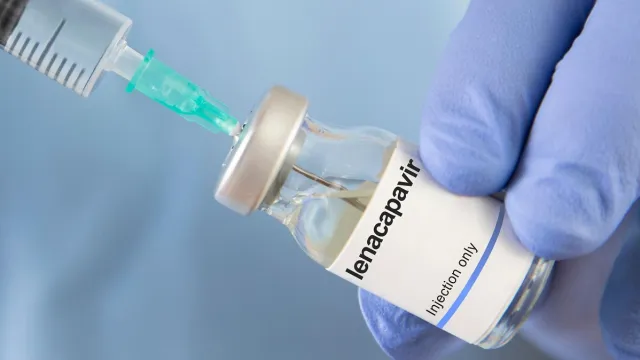

Kenya greenlights twice-yearly HIV prevention shot Lenacapavir

WHO says with just two doses per year, lenacapavir offers protectiong to people

News

•

Jan 05, 2026

Acid test for Kenya’s sugar factories’ leasing plan as Comesa safeguards end

Initiative to lift safeguards comes days after plan to lease Sony, Nzoia,

News

•

Dec 22, 2025

UjuziKilimo unveils AI-powered smartphone-based soil testing service

Each test analyzes over 13 critical soil parameters, including nitrogen,

Fact Check

View all

Fact check

•

Nov 01, 2024

ALTERED: This image isn’t of Rigathi Gachagua

The image has been doctored by adding the face of the impeached deputy president. This photo on Facebook purported to be that of the Deputy

Fact check

•

Nov 01, 2024

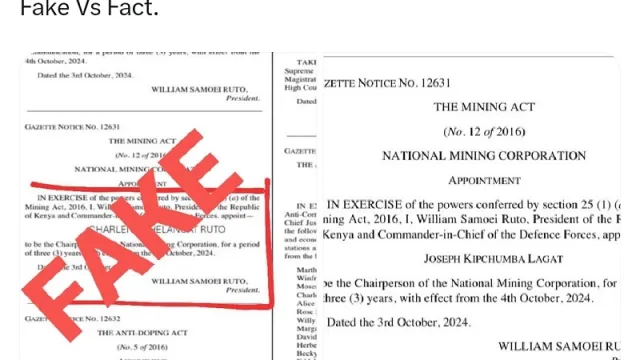

FALSE: Charlene Ruto isn’t chairperson of National Mining Corporation

Fact check

•

Nov 01, 2024

FAKE: This digital card on Charlene Ruto being endorsed for Deputy President position is fabricated

Fact check

•

Oct 28, 2024

FAKE: This Facebook page advertising paid tasks at Kenya’s Kilimall online shopping mall is a sham

Fact check

•

Oct 24, 2024

ALTERED: Donald Trump has not advised President Ruto on airport deal

Fact check

•

Oct 23, 2024

ALTERED: Father Charles Kinyua did not call Ruto a thief in his sermon

Corporate

View all

Corporate

•

Jan 06, 2026

Unlocking Kenya’s Next Phase of Growth

The next wave of progress will come not from more regulation, but from better, simpler enforcement of existing ones.

Corporate

•

Dec 18, 2025

Reflecting on a Landmark Year (2025): M-PESA, Partnership, and the Dawn of Fintech 2.0

Through Fintech 2.0 investments, Safaricom continued to modernise the

Corporate

•

Dec 17, 2025

How Safaricom Is Helping Enterprises Build Cyber Resilience

Organisations that prioritise resilience grow without interruption. And

Corporate

•

Dec 15, 2025

Why retirement planning is now a personal responsibility as family support declines

Young people who were once viewed as retirement plans now carry own financial

Advertisement

Life

View all

Life

•

Nov 26, 2025

Yesterday a turn boy, today a millionaire

Life

•

Nov 25, 2025

Going beyond the basics – the story of Human Needs Project in Kibera

Life

•

Nov 21, 2025

The Must-Have Tech Essentials for the Digital Mom Era

Life

•

Oct 21, 2025

Aga Khan University's Prof. Atwoli Takes Helm of World Health Summit

Sustainability

View all

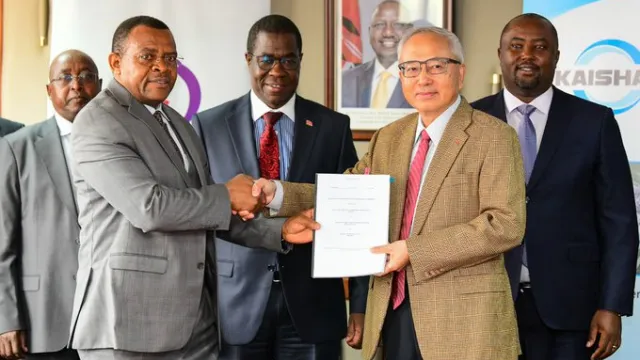

Sustainability

•

Nov 03, 2025

KenGen eyes Sh1.7 billion profit from green fertilizer factory

KenGen signs a 30-year partnership with China's Kaishan Group to tap steam to produce 300,000 tonnes of green fertilizer annually.

Sustainability

•

Oct 29, 2025

In Kenya, public concern for climate change drops sharply

Sustainability

•

Oct 21, 2025

Equity Afya clinics served 1.2 million patients in 2024

Sustainability

•

Oct 08, 2025

KCB Group deepens sustainable finance with Sh53.2Bn in green loans

Sustainability

•

Sep 24, 2025

Kenya and EU in push to speed up shift to clean energy future

Sustainability

•

Sep 10, 2025

Ethiopia urges Africa to form own path to combat climate change

Economy

View all

Economy

•

Jan 21, 2026

Nairobi stakes claim as Africa’s finance and crypto capital at Davos

Economy

•

Jan 20, 2026

Kalahari Cement rolls out Sh25Bn push to triple EAPC capacity

Economy

•

Jan 14, 2026

AGOA: Kenya gains fresh duty-free U.S. entry until 2028

Economy

•

Dec 19, 2025

Bankers seek PAYE reforms setting tax-free salary at Sh30,000

Markets

View all

Markets

•

Jan 19, 2026

Kenya Pipeline breaks decade-long IPO drought with Sh106Bn ambition

The govt is offering 11.8Bn shares, equivalent to 65% of Kenya Pipeline Company at KSh9.00 per share, aiming to raise KSh106.3Bn from the markets

Markets

•

Jan 16, 2026

Global online forex group Capital.com receives CMA nod to trade in Kenya

Markets

•

Jan 13, 2026

Mbadi defends Government’s 15% Safaricom sell-off to Vodacom

Markets

•

Dec 17, 2025

M-PESA propels Safaricom green bond retail uptake

Markets

•

Dec 17, 2025

Japan's Asahi gulps Diageo's EABL stake in KES296 billion deal

Markets

•

Dec 15, 2025

In a first in EA, Africa Logistics Properties Ltd Unveils Real Estate Investment Trust

Partner content

View all

Partner content

•

Jan 21, 2026

ABSA returns to power the 5th Sirikwa Classic Cross Country tour

Partner content

•

Jan 20, 2026

Njoroge Kibugu Surges Ahead After Round One of Absa Invitational Series at Karen

Partner content

•

Jan 16, 2026

Absa Bank Kenya recognised as a top employer for fifth year in a row

Partner content

•

Jan 16, 2026

Security guard turns millionaire in Safaricom Shangwe @25 campaign